Hayekian Realcoins and Prediction Markets

Creating currencies that stabilize purchasing power.

Welcome to the latest edition of The API Economy. Thanks for being here.

To support the API Economy, join the 12,093 early, forward-thinking people who subscribe for insights on the forefront of technology, crypto, AI, and other emerging trends.

Stablecoins today sit at just above $320 billion in total issuance, growing fast at a 50% 4 year CAGR. The vast majority of these stables are denominated in a single currency, the US dollar.

These stablecoins represent a superior form of the US dollar from a technological standpoint, but they still don’t solve for one of the biggest flaws in government-issued fiat: inflation and currency devaluation. In other words, technology today doesn’t solve the problem of maintaining the purchasing power of the dollar.

While stablecoins are unambiguously upgrading the grounding of our monetary system, a question still remains. Can stablecoins be composed with other primitives to solve currency devaluations?

Let’s dive in.

Apples to apples

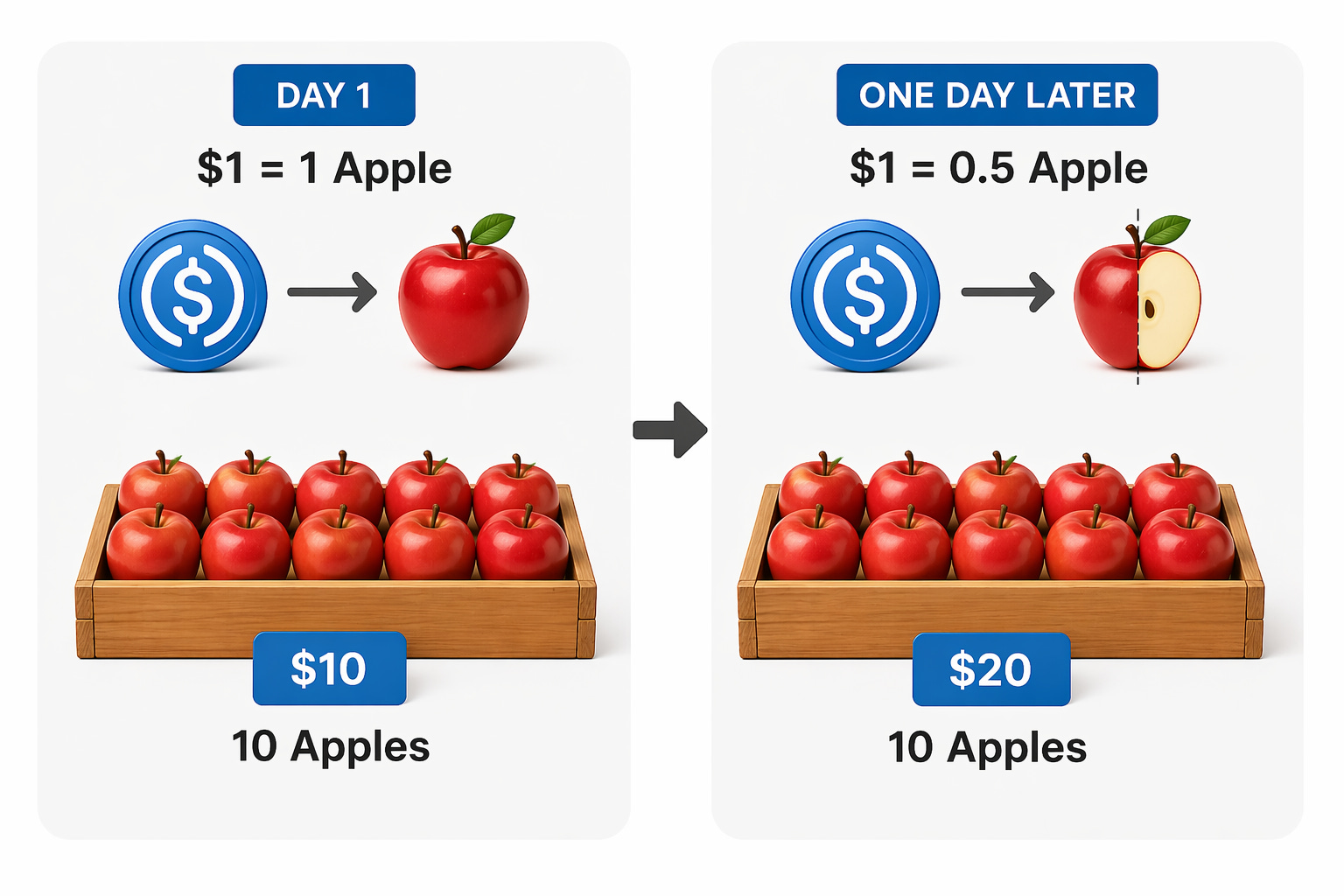

In its base state, value is not experienced as currency; it is experienced as goods and services. At a basic level, if a stablecoin user purchases 10 apples for $10 USD ($1 = 1 apple) and one day finds that the 10 apples cost $20 ($1 = 0.5 apple), there is a value loss of 50%. While your stablecoin stays worth $1, the goods you are buying are volatile.

If a traditional stablecoin maintain their dollar peg, but those dollars fluctuate in value, the question becomes: how do we create an instrument that stabilizes what those dollars can buy, the value itself?

The rise of prediction markets has been met with equal parts enthusiasm and disdain. Their potential as information aggregators is undeniable, but so is the speculative access and gambling they enable. The core innovation with prediction markets is not that they reveal information; it is that they expand the bounds of information that price discovery lends itself to.

This financialization of coveted, relevant information (interest rates, wars, weather) reveals potential for novel hedging strategies and end-user access to said strategies. The existence of hyper-localized prediction markets can translate into personalized “stores-of-value” that use outcomes to underpin value. We call these instruments realcoins.

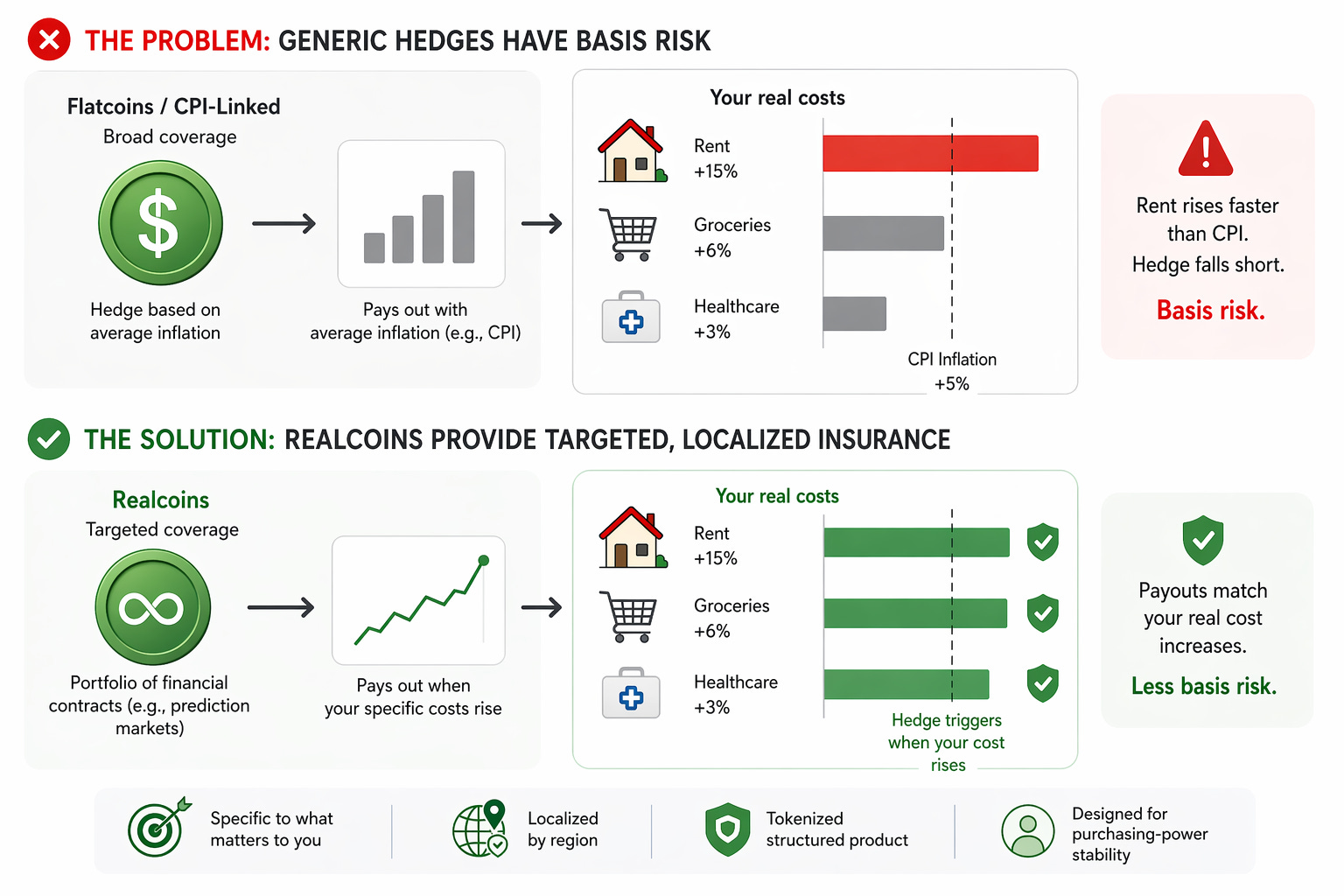

Realcoins aim to achieve value stability by holding portfolios of financial contracts, including prediction markets, that payout when the user experiences purchasing power erosion on goods and services most relevant to the user. The pursuit of purchasing-power stability is not new: flatcoins and CPI-linked currencies are being experimented with today. These instruments achieve broad coverage, but lack specificity - if your rent grows faster than CPI, the hedge is lost since it was generalized; this is known as basis risk. Realcoins attempt to bridge the gap by offering localized insurance as a tokenized structured product.

This outline is not meant to decry the proliferation of dollar-denominated stablecoins. It is an exercise to see if prediction markets can feasibly function as more than digital casinos, and to see if we can enable a currency that is more store-of-value than existing options.

Lineage

Friedrich Hayek, a stalwart of the Austrian school of economics, wrote “The Denationalisation of Money” in 1976. The pamphlet describes a competitive marketplace of privately issued currencies, where successful currencies best preserve value over time. He believed that institutions would find, through experimentation, that a basket of commodities forms the ideal monetary base. Hayek’s ideas were rooted in a distrust of the government and a belief that economic order arises from decentralized markets rather than central planning.

Aspects of Hayek’s vision echo Bitcoin, but speculative capital, high volatility, and surrounding derivative markets render it ill-suited for the “store-of-value” function of money. The US dollar addresses the denomination problem, but due to centralized planning and perverse incentives (deficits, seigniorage, political accommodation of loose policy) driving inflation, it fails to solve the purchasing-power problem. Hayek had identified the destination, but lacked the mechanisms in the 1970s.

Tectonic shifts in finance reveal new opportunities. Stablecoins prove that privately issued digital money can achieve adoption at scale. Decentralized finance demonstrates that financial contracts, including derivatives and structured positions, can be composed and executed programmatically without traditional intermediaries. Prediction markets create liquid, tradeable claims on real-world outcomes, including those that determine purchasing power. A realcoin issuer that operates as a licensed entity, holding a portfolio of prediction market positions on behalf of users, sits at the intersection of all three.

Vitalik Buterin, co-founder of Ethereum, independently proposed this idea, describing the creation of prediction markets on all major categories of goods and services that people buy. In his outline, an LLM would analyze user expenses and create a personalized basket of prediction market shares representing expected future expenses. For many, rent is the largest expense, and also the one most exposed to inflation. Can prediction markets help maintain the ability to pay rent?

Prediction Markets as Localized Insurance

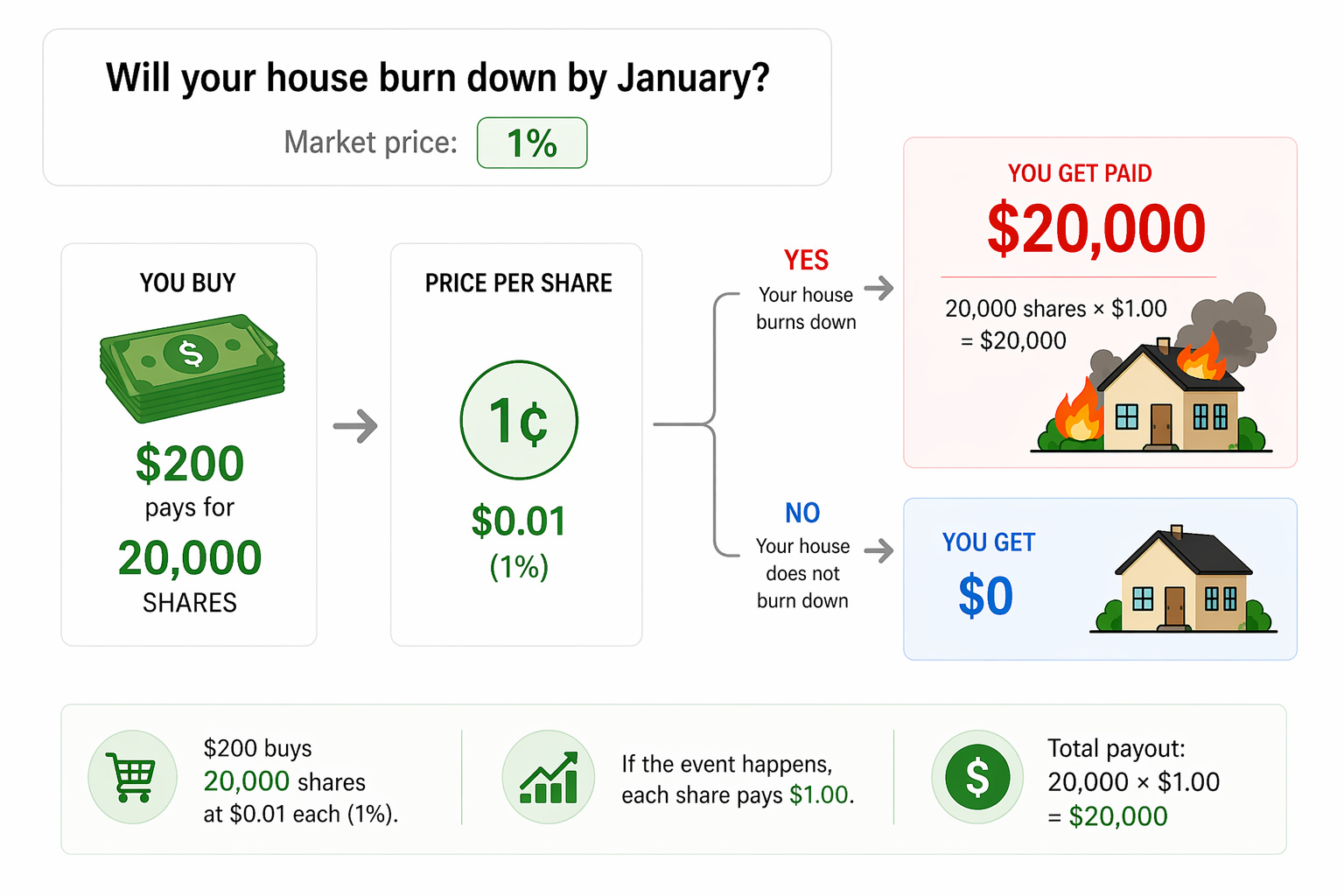

Insurance exists so that when the thing you care about (experienced value) gets worse, you remain stable in financial terms. You pay a premium, and in return, if life doesn’t go as planned, you are made whole. If a prediction market prices “Will your house burn down by January” at 1%, $200 buys you 20,000 shares, and you are paid out $20,000 if your house burns down.

As such, prediction markets functionally replicate insurance. Notably, insurance requires an “insurable interest” - you can only insure something that you own and are the beneficiary of. Prediction markets have no such restriction. To hedge an outcome, one no longer needs an underwriter, claims process, or tailored policy; all that’s needed is a liquid market on an outcome tied to the cost of living.

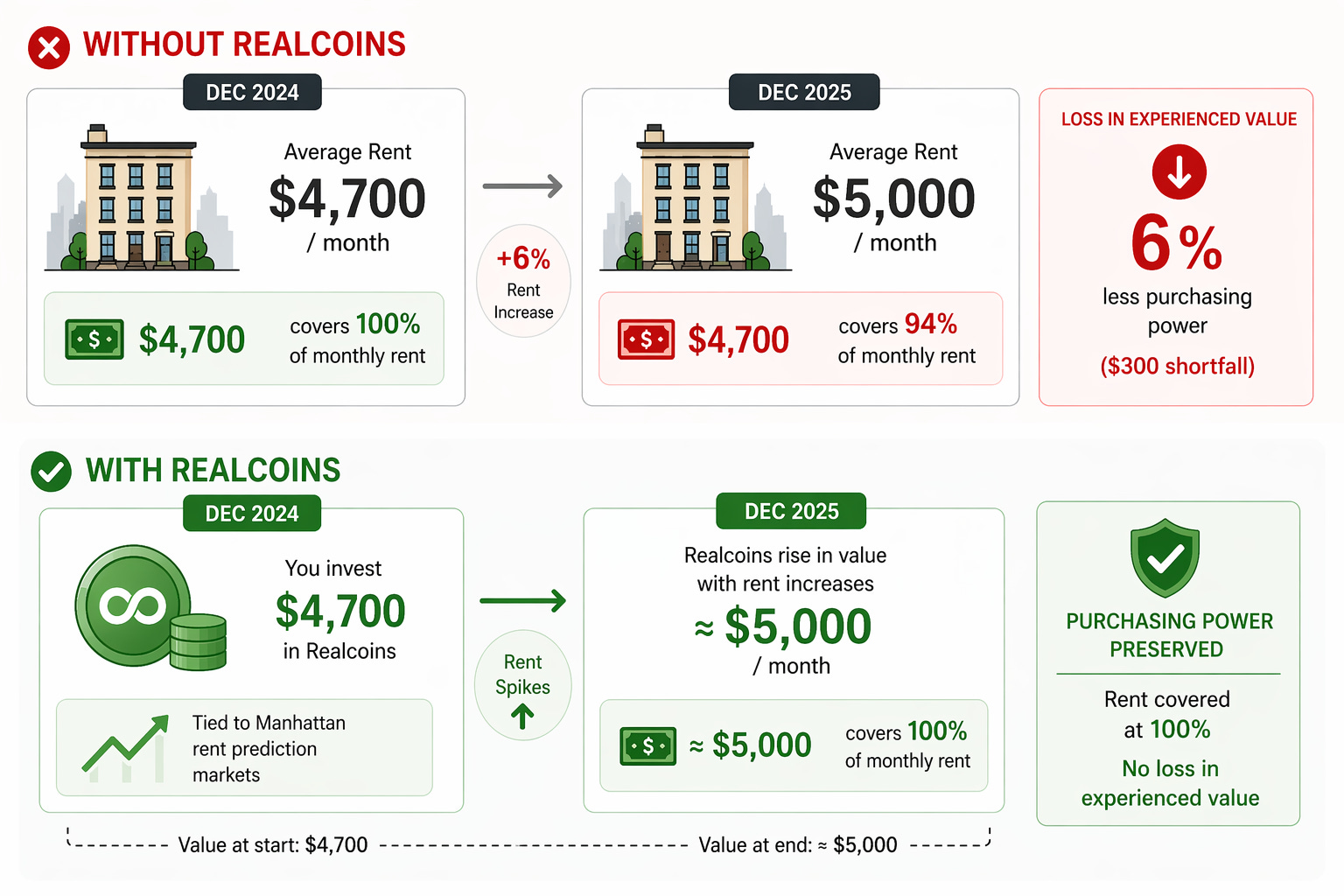

For New Yorkers, rent increases are a critical and often underestimated driver of purchasing power erosion. As of December 2025, average rent was at around $5K monthly, up 6% from $4.7K in December 2024. 4.7K USD covered 100% of the monthly rent in 2024 but only 94% in 2025, a direct loss in experienced value. Had the renter invested $4.7K in 2024 into realcoins tied to Manhattan rent prediction markets, the underlying contracts would rise in value with rental spikes, preserving rental purchasing power. This core mechanism makes realcoin values positively correlated to the cost-of-living.

Realcoin holders do not speculate on these outcomes; they hedge them. A renter could see rent increases regardless of whether or not they buy shares. A sports speculator has no linkage to the outcome of a sporting event. The speculator assumes financial risk proactively; the realcoin holder experiences it regardless. Buying prediction market shares does not introduce new risk to realcoin holders; it offsets risk already present in their lives. This extends into expectation setting as well - realcoin holders expect to lose value should outcomes go their way, since purchasing power was preserved, and the hedge was unnecessary. A speculator expects to gain value if outcomes go their way. This inversion characterizes the intent distinction between gambling and hedging and can underpin the case for prediction markets as legitimate financial primitives.

A Manhattan renter hedges against shelter inflation. An online merchant hedges against Cloudflare downtime. A small business owner in a flood-prone area hedges against weather disruption. Each is using the same primitive: a liquid, outcome-based financial contract, to stabilize a different dimension of their economic life. Realcoins aggregate these primitives into a single instrument calibrated to a user’s actual expenses.

Realcoin design options

There is no single design that accomplishes a realcoins purpose. Operationalizing realcoins implies finding financial contracts that pay out when the cost of living rises and are dependent on existing markets, liquidity, and the legal backdrop that issuers operate in.

Design 1: Binary Prediction Markets

The simplest design is where a realcoin is backed by shares in a binary Yes / No prediction market where the outcome is tied to cost-of-living thresholds. Suppose a market in New York rent resolves “Yes” if the median Manhattan rent exceeds $5K and is currently priced at 35%. If your rent is $4.7K and you purchase $4.7K worth of shares at 35%, you own 13.4K shares. If the market resolves and the oracle reports that the median rent exceeded $5K, you are then paid out $13.4K, offsetting the higher rent you now owe. If the market resolves to “No”, your shares are worth nothing, and you lose the $4.7K investment, but have paid for protection that was not necessary; this is how insurance works. The true design limitation is the scenario where your rent rises from $4.7K to $4.9K, eroding purchasing power without the hedge activating.

Binary markets are easy to understand, easy to price, and already exist. A basket of five to ten markets covering rent, groceries, electricity, healthcare costs, and more could be constructed on a platform that supports cost-of-living markets. The limitation is a lack of precision. Coverage exists, but it is not comprehensive enough to be reliable for everyday users. Binary markets achieving popularity lay the foundation for more elegant solutions.

Design 2: Parametric / Scalar Markets

Parametric prediction markets address the risk in binary markets by tying payouts to an index value rather than a binary threshold. Continuous parametric markets that smoothly change payout with the index do not yet exist, but approximations of this structure using nested binary markets as “rungs” of a prediction ladder are active today.

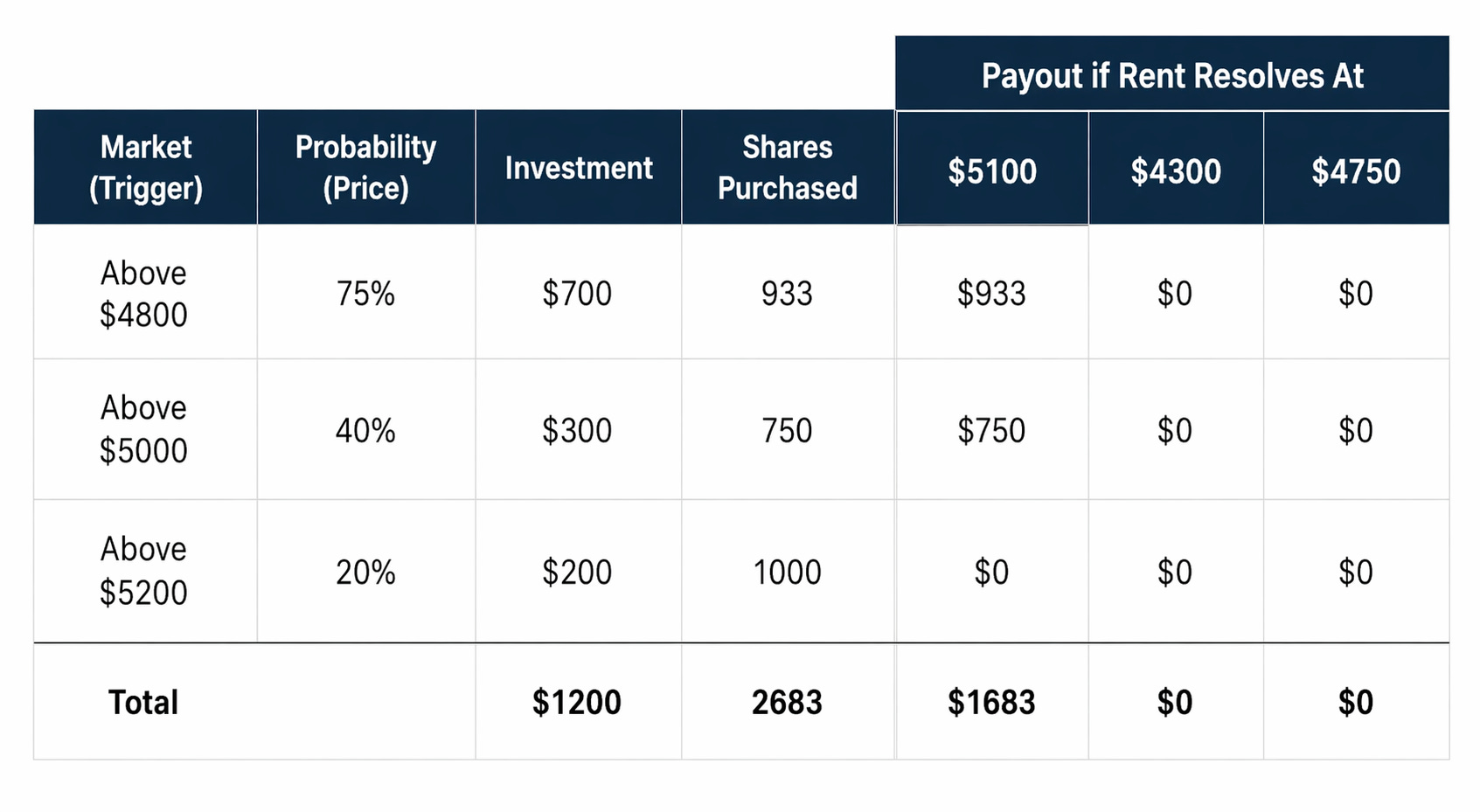

A pseudo-parametric market for NYC rent might look like a 3 rung ladder where each median rent tier has different probabilities and different payouts. For instance, you invest $1200 into the NYC rent realcoin, backed by markets with the following parameters:

The quantity of shares purchased is the Investment amount divided by the price, expressed as cents.

In the scenario that rent falls from $4.7K to say, $4.3K, you lose the $1.2K invested principal. All 3 markets resolve to “No”, and the shares purchased are all worthless. Simultaneously, you have also seen an increase in purchasing power, since rent has fallen. Payouts are meant to correlate with experienced value, so the realcoin accomplishes its purpose, though the nominal invested value is lost entirely.

Parametric markets are critical to ensuring realcoins are commercially feasible, though current implementations come with limitations. Leveraging nested binary markets means payouts only happen at the rungs, and never in between. For instance, if rent landed at $4750, purchasing power would be eroded, but no insurance was inherited since none of the markets resolved “Yes”. Widely spaced thresholds in such markets pose risks to realcoin holders. Tighter rung spacing enables granularity, but also higher operational costs, which may be well worth it.

Design 3: Yield-bearing collateral and prediction market exposure

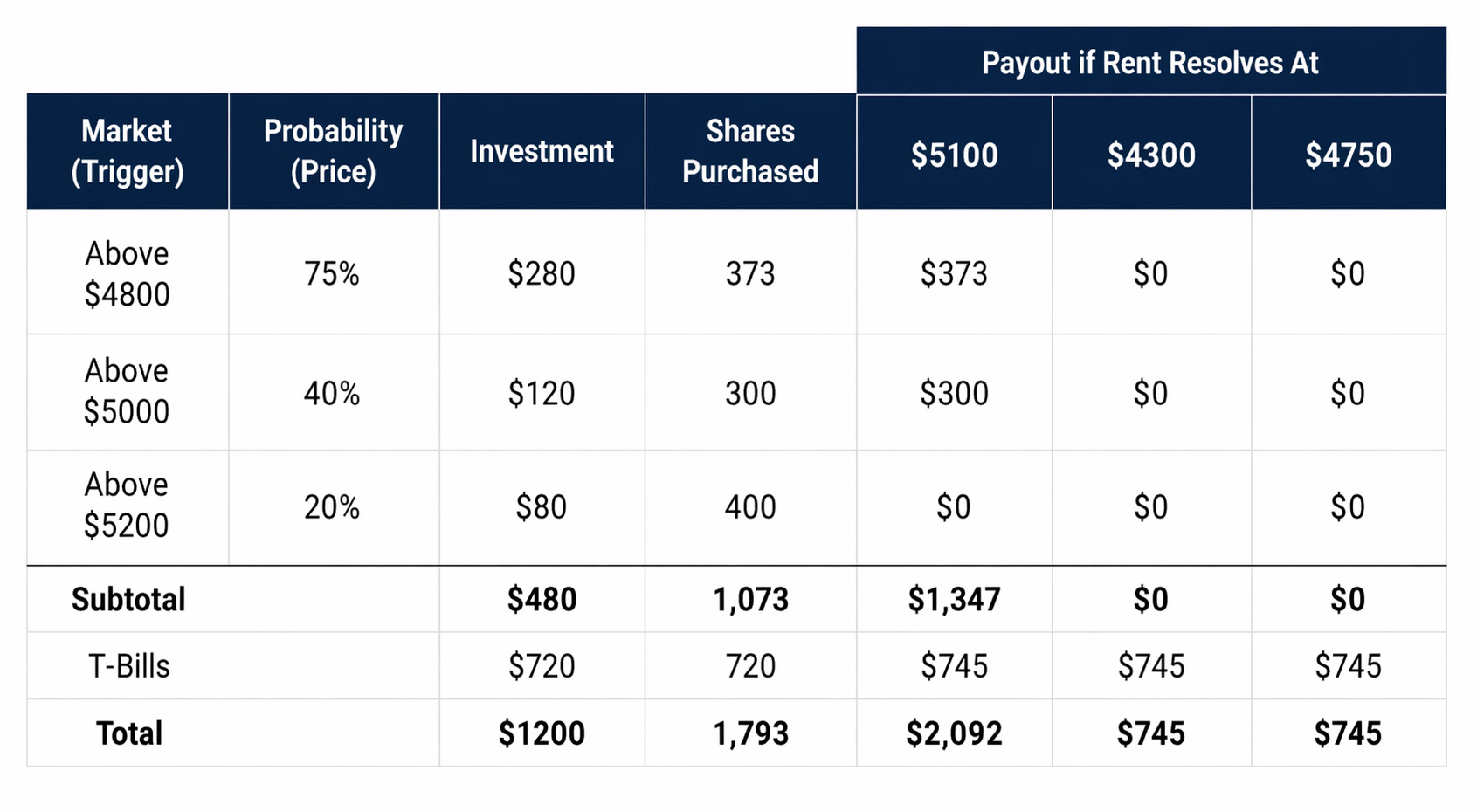

Designing a realcoin in which the full nominal investment can be lost is difficult to market to retail holders. One could address this by diversifying the reserve composition to include yield-bearing collateral, such as a money market fund earning the risk-free rate. If positions pay out, the combined instrument protects purchasing power. If they don’t, you still earn yield on a portion of the deposit, a better outcome than holding fiat or stablecoins. This income-generating base can offset the operational costs associated with managing realcoin reserves and diversify exposure, with the remainder of reserves invested in prediction markets. Such a structured product could be composed of 60% T-Bills and 40% prediction market shares.

In this setup, the principal loss in the downside scenario is only 38% of the total investment amount, while still maintaining purchasing power. Unlike the parametric-only design, the gap scenario is no longer a total loss. This structure of a money market fund with an attached hedge has established legal precedence and frameworks. What is novel is the prediction market hedging layer, which may not be regulated like traditional instruments.

Looking Ahead

The usefulness of a realcoin is predicated on market specificity, adequate liquidity, and legislative clarity. Without sufficient specificity, there could be gaps between insured outcomes and experienced outcomes (basis risk), and without active buyers and sellers, markets cease to exist. A national shelter CPI index does not track Manhattan. The hedge applies, but is closer to an inflation-linked bond than to bespoke insurance. Volumes for cost-of-living markets pale compared to those for sports and elections. These markets also require naturally opposing buyers and sellers who take the other side of each position. Closing these gaps is the long-term product problem realcoins need to solve.

Hayek’s insight was not that any particular currency would win, but that competitive markets would discover which instruments best preserved purchasing power over time. Realcoins are an entry into that competition. They require liquid markets, honest oracles, and users whose experienced value is worth hedging. The instruments that best track what users actually spend money on will attract holders; those with persistent basis risk or thin liquidity will not. Issuers competing on composition, rung structure, and collateral ratio, not to mention partnerships for market access and market making, should drive product outcomes that unlock value stability for end users.

The conceptual case for realcoins does not depend on that maturity being achieved immediately. The tools to solve for value exist today.

Disclaimer: This month’s edition of The API Economy has no direct affiliation with Circle or any other company mentioned. Both Shaurya and I are employed by Circle at the time of this writing, but the views in this essay are our own personal opinions and don’t represent the views of Circle.

| A guest post by

|