Stablecoins | The Monetary Upgrade

Stablecoins are becoming the digital currency used to reshape global finance and commerce as we know it.

Welcome to the latest edition of ‘The API Economy’ — thanks for reading.

To support The API Economy, be one of the 8,420 early, forward-thinking people who subscribe for monthly-ish insights on the API economy, crypto, stablecoins, and more emerging trends.

No innovation has captured the imagination & potential of both the technology and finance worlds like stablecoins have.

These digital currencies, designed to maintain a stable value relative to a reference asset (most of the time a fiat currency like the US dollar), have emerged as a bridge between the traditional financial system and blockchain technology.

This week’s news of Stripe acquiring Bridge has sent ripples throughout the tech world and opened people’s eyes to the potential stablecoins to pave a new monetary superhighway.

Let’s dive into what stablecoins mean for the future of money.

The meteoric rise of stablecoins

There’s a saying that the ultimate form of sophistication is simplicity.

With all of the complexities that come with crypto at times, stablecoins are about as simple as you can get in principle — it’s digital money that combines the benefits of crypto with the stability of traditional finance.

It will all seem obvious in hindsight, but we’re at an inflection point for money.

Stablecoins aren't just an improvement on existing systems; they're laying the groundwork for an entirely new internet-based financial system.

As a result, the market cap of fiat-backed stablecoins has swelled from its conception in 2018 to over $220 billion as of February 2025.

To put this in perspective, that's more than the GDP of many countries.

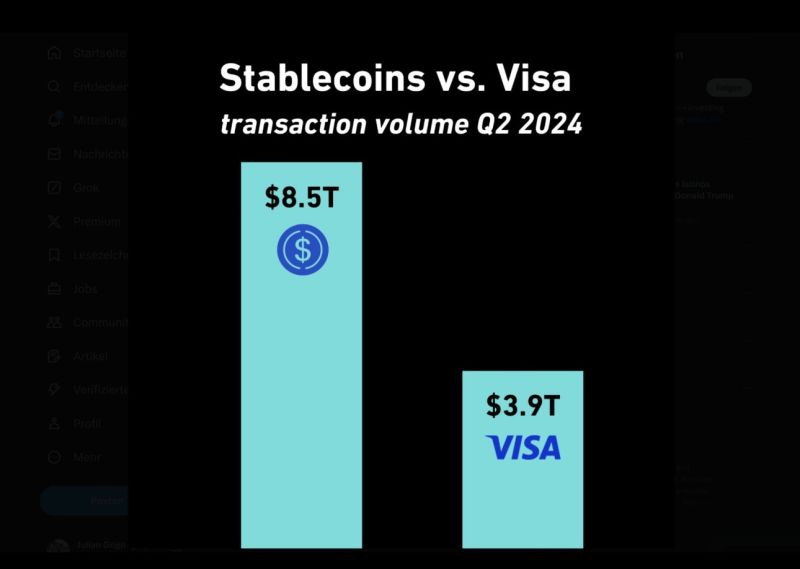

And these stablecoins aren’t sitting idle. In Q2 alone, stablecoins processed more transaction volume than Visa by nearly 2x, with transaction volumes often exceeding trillions of dollars a month.

These levels of growth for a technology invented only 6 years ago are staggering.

The business of stablecoins

Why are stablecoins a good business, and how do they make money?

Stablecoins generate revenue by investing their reserves 1-for-1 in interest-bearing assets, such as treasury bills and other short-term investment vehicles. The interest earned from these investments provides a source of income for the stablecoin issuer.

This innovative investment strategy has led to stablecoin issuers, in aggregate, becoming one of the biggest holders of US treasury bonds, holding more than countries like Germany, Mexico, and the Netherlands.

But stablecoins are just beginning to realize their potential.

Consider this: the global money supply (M2) is estimated to be around $129 trillion.

We’ve only begun to scratch the surface of updating the financial system through stablecoins.

Outside of M2 money supply, here are the sizes of some other markets that stablecoins are poised to improve:

Foreign Exchange (Forex): $8 trillion moves between different currencies every single day. It’s the biggest market in the world. It’s about 30 times the daily global GDP.

Once we have deeper liquidity for more currency-backed stablecoins around the world, digital foreign exchange through stablecoin swaps will quickly begin to change the way money moves between currencies today.

Global Remittances: In 2023, the value of remittances worldwide amounted to an estimated $883 billion and is expected to reach $913 billion by 2025.

Stablecoins make cross-border payments as easy as sending a text or an email by offering faster, cheaper, and more seamless transactions.

Payments: The global payment market is valued at $2.64 trillion as of 2023 and is expected to grow to $4.78 trillion by 2029. Credit card processing fees vary by region, payment method, and transaction type but generally range from 1.5% to 3.5% of the transaction amount. The average global fee for processing credit card transactions in 2024 is around 2.4% of the transaction value.

Stablecoins have the technological ability to streamline payment workflows to make them much more efficient.

If stablecoins were to capture even a small fraction of these antiquated markets, trillions of dollars would flow into digital currencies that would radically improve the financial system.

The miracle of money

Why is money based on the internet so important?

Similar to water, money permeates through our society, nourishing economic activity.

It seeks the path of least resistance, much like water flowing downhill. Just as water is essential for life, money is the lifeblood of commerce, enabling transactions and storing value.

It's important to understand the fundamental functions of money itself to help understand the value of stablecoins.

Money, in its essence, exists to solve a basic problem: how to efficiently exchange value in a complex society. Economists have long recognized three primary functions that define money:

A store of value

A medium of exchange

A unit of account

These functions form the bedrock of any monetary system, allowing individuals and societies to save, trade, and measure economic value over time.

By design, stablecoins aim to fulfill these same core functions, but in the digital realm, they offer improvements over traditional forms of fiat money.

Store of Value

One of the most immediate and obvious use cases for stablecoins is as a store of value, particularly in countries with unstable currencies or limited access to the global financial system. For someone living in a country with high inflation or strict capital controls, holding stablecoins pegged to the US dollar or Euro can be a lifeline to protecting their hard-earned capital.

Nearly 75% of all physical 100-dollar bills are held offshore, representing over $1.5T in value. Now, people can access dollars or other currencies of any amount 24/7/365 in a digital form factor through stablecoins.

Medium of Exchange

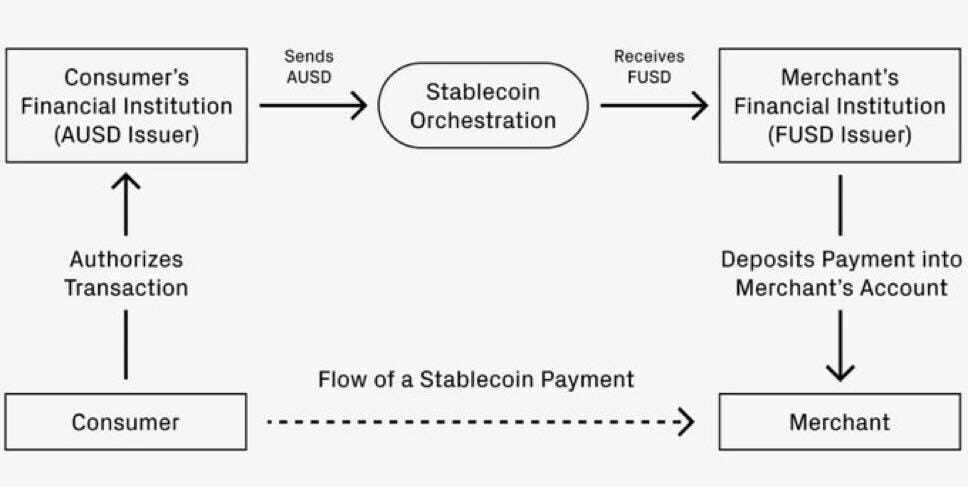

As a medium exchange, stablecoins have an opportunity to replace existing flows through their efficiency and programmability. In every single workflow that has a middleman facilitating and taking parts of a transaction, stablecoins have the opportunity to abstract away and streamline payment flows.

According to McKinsey research, in 2023, the global payments industry handled 3.4 trillion transactions, accounting for $1.8 quadrillion in value and a revenue pool of $2.4 trillion. By streamlining these payments, stablecoins chip away at that $2.4 trillion global payment tax, making payments more efficient for everyone.

Stablecoins are already overtaking the majority of crypto volumes and will soon do the same for other industries.

Unit of Account

While stablecoins are already useful as a store of value and medium of exchange, their potential as a unit of account is still largely untapped. As more businesses and individuals become comfortable with stablecoins, we could see them being used to price goods and services, especially in international contexts.

According to SWIFT, the US dollar accounts for over 80 percent of trade finance due to the fact that the majority of commodity trade continues to be invoiced and settled in dollars.

The global trade finance market was evaluated at $10.5 trillion in 2023 and is slated to hit $13.6 trillion by the end of 2032. With a CAGR of nearly 2.94% between 2024 and 2032, this represents an enormous opportunity for stablecoin settlement.

In short, stablecoins are still early.

Internet money is just better

Apps like Venmo and Cash App have revolutionized peer-to-peer payments within the United States, making it simple to split a dinner bill or pay rent.

However, these solutions are largely domestic. There's no "global Venmo" that allows for quick, easy, and cheap international transfers.

This is where stablecoins shine. They offer an inherently global solution, operating 24/7 and not constrained by national borders or banking hours. With stablecoins like USDC, sending money anywhere in the world becomes as easy as sending a text, and often at a fraction of the cost of traditional international wire transfers.

Post-Dencun upgrade on Ethereum in March has led to the average cost on L2s like Base falling below $0.01. It is nearly instant and available anywhere in the world.

Brian Armstrong, the CEO of Coinbase, recently spoke at a Goldman Sachs conference where he said:

“What I’m really happy to report is that we’ve now gotten that under one second and $0.01 for a transaction anywhere in the world globally.

That makes crypto, I think, the best payment rail globally to date. There’s some in the traditional financial system. There are some payment rails that are very fast, like credit cards, but they’re expensive, 2%. There’s some that are very cheap, like ACH, but they’re very slow.

Two to three business days. Right? And there’s some that are very fast and cheap, like WeChat payments, but they’re only in one country, China. Crypto, crypto rails on layer two, like base, are now the only ones I know of that check all three of those boxes. They’re fast, cheap, and global.

And that’s partly why I think we’ve seen that 200% to 300% increase year-over-year in stablecoin transaction volume. So that’s really powerful. It’s not just unlocking payments. It’s actually starting to unlock another category of applications.

So, an example would be, if you had fast, cheap, and global payments, what might that allow people to do? Maybe, sometimes on social media, people click the like button or they upvote upload something. You know, why can’t that be a small transaction? Right? Today in the US., people get paid every two weeks for their paycheck. Why shouldn’t you get paid every hour?

Maybe, this whole idea of payday lending could go away. Right? Or every minute. And so if the world had a fast, cheap, global financial system that was decentralized, not controlled by any one country, I think a lot of friction would get taken out of the economy and you’d see a lot of growth. Even small amounts of friction that are reduced, you see huge increases in adoption. Like for instance, text messages used to cost $0.25.

There was about 25 billion text messages a year at its peak. Today with WhatsApp and iMessage and things that are, these are now free, there’s hundreds of billions of messages sent every day. So you can get an order of magnitude increase in activity just by taking out a small amount of friction. And that happened in messaging, that’s now going to happen in payments.”

Said more explicitly, stablecoins like USDC on L2s have become the most efficient payment rails in the world.

Let that sink in…

As more applications integrate stablecoin functionality, we'll likely see network effects. Each new app that adopts stablecoins increases the utility of the entire ecosystem, incentivizing further adoption and innovation.

Network effects occur when a product or service becomes more valuable as more people use it. Think about social networks like Facebook or communication tools like WhatsApp – their value increases exponentially with each new user.

Stablecoins have the potential for incredibly strong network effects.

As more people start using stablecoins, more businesses will accept them, and as more businesses accept them, more people will want to use them.

This virtuous cycle could lead to rapid, widespread adoption that happens at a rapid pace.

Out with the old, in with the new

When we look at the stablecoin landscape, people often compare it to the early days of the Internet. Back then, it was hard for many people to grasp just how transformative the technology would be. We're in a similar place with stablecoins.

In an episode of The Money Movement with Jeremy Allaire, Chris Dixon said:

“All new technologies tend to do two things. They tend to do old things better and new things you couldn’t do before. What blockchains really are is a new way to build internet services that are architected in a way where there’s no gatekeeper or no toll keeper.”

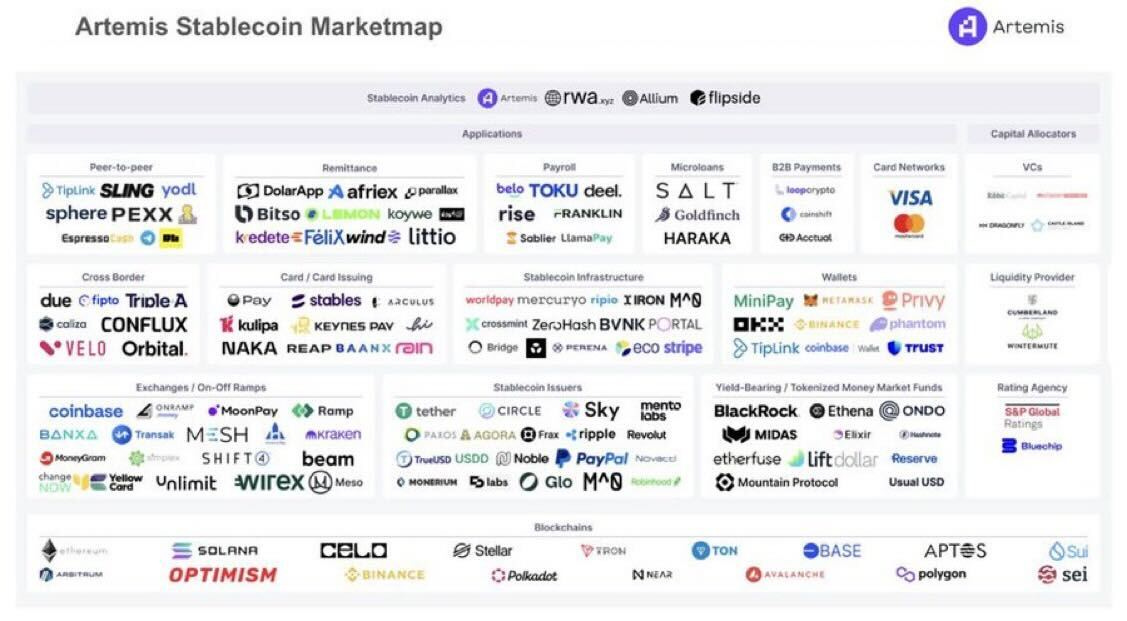

Stablecoins represent a massive opportunity for entrepreneurs, developers, and innovators. The companies and protocols that successfully navigate this space could become the financial giants of tomorrow.

Here’s a list of just some of the companies innovating in the stablecoin ecosystem today:

The potential is enormous. Stablecoins have the power to remake the financial system in a way that's more open, efficient, and inclusive.

They could be the key to unlocking global financial inclusion, enabling new business models, and creating a more interconnected global economy.

And don’t blink because this growth is happening rapidly, with several stablecoins growing to over $1 billion in supply in less than a year.

There are also now over 76 stablecoin projects, which are above $10 million in supply.

The potential for growth is not just large; it's transformative on a global economic scale. And we’re still just getting started.

We're standing at the threshold of a new era in finance. The stablecoin revolution is just beginning, and I, for one, can't wait to see where it takes us.

Until our next adventure.

Disclaimer: This month’s edition of The API Economy has no direct affiliation with Circle, or any other company mentioned. I am employed by Circle at the time of this writing, but the views in this essay are my own personal opinions and don’t necessarily represent the views of Circle.

Note: Thanks to all of the people who have consistently conducted quality stablecoin research, including but not limited to — Nic Carter, Cuy Sheffield, Jon Ma (and the entire Artemis team), Simon Taylor, and Electric Capital.

RLUSD let’s go

Fantastic article. This is exactly why we are pioneering "global Venmo" at psifi.app